Retail in the Red: BDO Bi-Annual Bankruptcy Update - 2H 2023

An overview of the state of U.S. retail, including bankruptcies and store closings, for the second half of 2023, and a forecast for 2024.

2023 was a year of economic growth, job creation, low unemployment, and easing inflation. These factors contributed to strong 2023 retail holiday sales. Some of the key issues that challenged the retail industry in 2022, such as supply chain slowdowns and excess inventory, subsided in 2023. Despite the easing of these challenges, 2023 was also a year marked by cautious consumers who searched for discounts and focused their spending on essential goods over discretionary purchases, battling both high prices and high interest rates. Price-conscious consumers contributed to the continued success of dollar stores and discounters, while some discretionary retailers suffered. Going into 2024, historically high consumer debt may handcuff consumer spending. BDO’s Spring 2024 Retail in the Red Report examines 2023 retail bankruptcy filings, store opening and closing, and macroeconomic data, and provides our predictions for retail in 2024.

Retail Bankruptcy Update

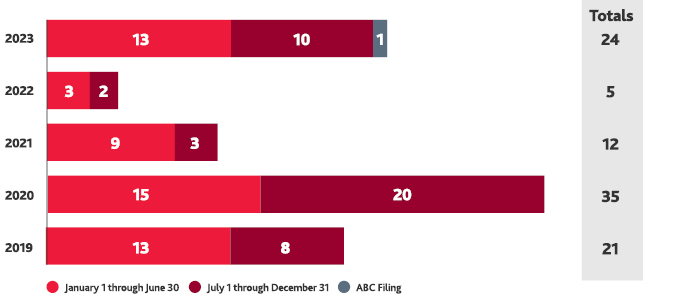

Retail bankruptcies picked up in 2023, with 10 new filings in the second half, plus the filing of an Assignment for the Benefit of Creditors (ABC) by the online apparel retailer Zulily, resulting in a total of 24 filings (including the ABC) for the year. This is a marked increase from the past two years and more in line with the number of annual filings seen prior to the pandemic.

Retailers That Filed for Bankruptcy in the Second Half of 2023k

| Company | Filing Data | Description | Bankruptcy Strategy | Bankruptcy Result or Latest Intent | Stores as of Petition Date | Store Closures Announced | |

| 4th Quarter | Zigi USA | 12/31/23 | Footwear | TBD | TBD | 0 | 0 |

| Hello Bello | 10/23/23 | Baby Care Products/Apparel | Asset sale | $65.8 million sale to stalking horse bidder, Hildred Capital Management affiliate. | 0 | 0 | |

| Z Gallerie | 10/16/23 | Homefurnishings | Asset sale | Approval to sell eCommerce assets to Karat Home Inc for $7.2 million. Wind down operating store and liquidate inventory. | 21 | 21 | |

| Rite Aid | 10/15/23 | Pharmacy | Dual sale processes for retail business and the Elixir pharmacy services business; close 400 stores. | Sold Elixir pharmacy benefit management business to MedImpact for $567.5 million. Retail business to be sold either to Lenders via credit bid or by auction. | 2,100 | 425 | |

| Shift Technologies | 10/09/23 | Automotive | Wind down business and liquidate assets. | Working with Hilco Streambank to auction various IP assets. | 2 | 2 | |

| 3rd Quarter | Noble House Home Furnishings | 09/11/23 | Homefurnishings | Asset sale | Sold assets to stalking horse bidder and DIP financing lender GigaCloud Technology. | 1 | 0 |

| Soft Surroundings (Triad Catalog Company) | 09/10/23 | Apparel | Asset sale | Sold online retail business to Coldwater Creek to continue as going concern and brick-and-mortar operations will be liquidated. | 44 | 44 | |

Off Lease Only | 09/07/23 | Automotive | Complete wind-down and allow it's lender to collect proceeds from vehicles securing a credit facility. | Converted to Chapter 7 liquidation. | 6 | 6 | |

The Mitchell Gold Co | 09/06/23 | Homefurnishings | Asset sale and liquidation | Stalking horse bid for assets rejected and DIP lenders pulled support. Converted to Chapter 7. | 30 | 30 | |

| Benitago | 08/30/23 | ECommerce | Asset sale | Confirmed plan of reorganization providing debt for equity exchange. | 0 | 0 |

Companies that filed for bankruptcy in the second half of 2023 included one retail pharmacy giant (Rite Aid), and various small retailers, including e-commerce and direct-to-consumer retailers (Benitago and Hello Bello), two automotive companies (Shift Technologies and Off Lease Only), and discretionary retailers selling home furnishings and apparel. The online apparel retailer Zulily commenced an ABC in December 2023 to wind down its operations, including the sale of $85 million of inventory and fixed assets located in two 775,000 square feet fulfillment centers.

The increase in bankruptcy filings in 2023 is likely due to several factors, including high interest rates, higher operational costs due to inflation, and the tightening of discretionary spending by consumers, resulting in a reduced ability for distressed retailers to obtain financing.

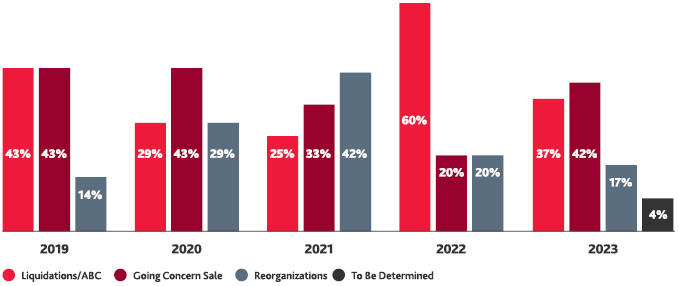

The outcome of retail bankruptcy filings between liquidations, sales, and reorganizations in 2023, as a percentage of total bankruptcies, also closely resembled the mix of bankruptcy outcomes seen pre-pandemic. In 2020 and 2021, we saw a trend toward reorganizations, whereas in 2022, there was a spike in liquidations. Retailers were more likely to reorganize prior to 2022 while interest rates were still low and lenders provided leeway. Times were less forgiving in 2022, with interest rates rising quickly and retailers facing huge amounts of excess inventory, leading to a preponderance of liquidations. In 2023, we saw a return to the 2019 distribution of bankruptcy outcomes, as supply chain and macroeconomic headwinds shifted. It is notable that with present interest rates much higher than in 2019 — a condition that would normally contribute to an increase in liquidations — we are not seeing more liquidations. This a trend we will continue to watch closely.

Outcome of Retail Bankruptcy Filings in BDO Retail in the Red Reports

| 2023 | 2022 | 2021 | 2020 | 2019 | Total | |

| Liquidation/ABC | 9 | 3 | 3 | 10 | 9 | 33 |

| Going Concern Sale | 10 | 1 | 4 | 15 | 9 | 38 |

| Reorganization | 4 | 1 | 5 | 10 | 3 | 23 |

| To Be Determined | 1 | 0 | 0 | 0 | 0 | 1 |

| Total | 24 | 5 | 12 | 35 | 21 | 97 |

Store Openings and Closings

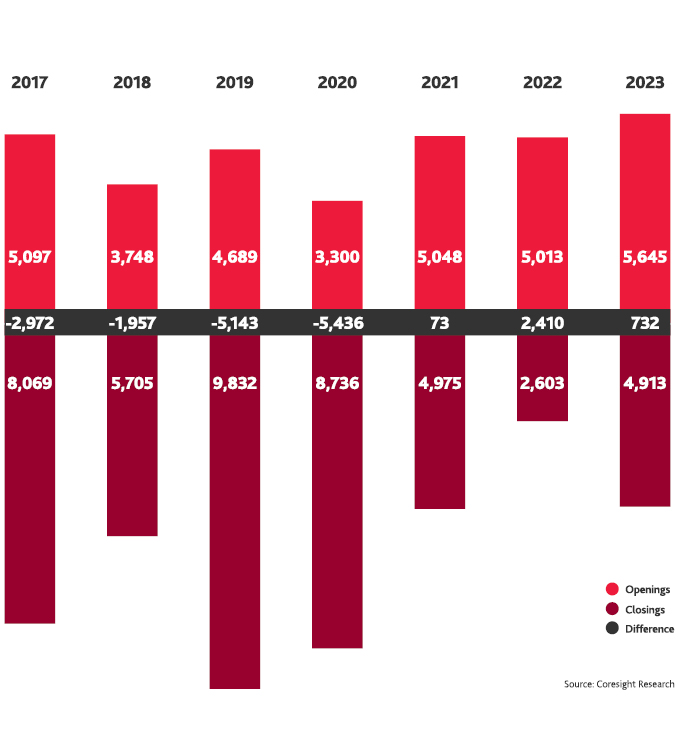

Except for Rite Aid, bankruptcies in the second half of 2023 did not result in many store closings. Net closings substantially exceeded store openings through 2020. However, since 2021, net store openings have exceeded closings as shown in the following chart:

Most store openings are by dollar and discount stores. Price-conscious consumers continue to be drawn in by low-price essential goods and groceries. For example, Dollar General has announced 800 new stores slated for 2024. Additionally, convenience store counts have also grown, increasing by 1.5% in 2023 from the prior year (2024 NACS/NIQ Convenience Industry Store Count).

There was a net opening of approximately 2 million square feet of retail space in 2023, but there was also an estimated 10% reduction in the average store size. An estimated 88.0 million square feet of retail space closed, with an average store size of 17,921 square feet, while 90.1 million square feet of new retail space opened, with an average store size of 16,136 square feet (Coresight Research). According to CoStar Group, store sizes by square footage are the smallest they’ve been in at least 17 years. Shrinking physical store square footage is tantamount to store closings as retailers replace large-format stores with small-format stores. Additionally, some traditionally mall-based retailers are shifting to neighborhood strip centers to take advantage of high-traffic locations with lower rent costs. Recent retailer store announcements include:

![]()

Macy’s has closed 80 department stores since Feb. 2020 and has since opened a dozen small-format stores that are 30,000 to 50,000 square feet (one-fifth the size of Macy’s mall locations) and plans to add an additional 30 locations by the end of 2025.

![]()

Nordstrom announced plans to open 23 Nordstrom Rack stores, in mostly suburban markets, through spring 2025, with locations ranging from 23,000 to 36,000 square feet.

![]()

IKEA opened more than 70 new, mostly small-format stores in 2023.

![]()

Bath & Body Works plans to have two-thirds of its stores outside of malls as part of its long-term strategy, as off-mall sales performance exceeded in-mall stores.

![]()

Walmart announced a 5-year plan by 2029 to convert 150 locations to new concept stores featuring improved layouts, expanded product selections, and new technology to add to the consumer shopping experience.

![]()

CVS is rationalizing its store base and plans to close dozens of pharmacies located within Target stores in early 2024.

SHARE